The game of two halves: an elegant two-step process designed to cut losers, run winners, while maintaining conviction

In every hospital around the world, there is an unwritten rule: surgeons should not operate on their own children. There is no such thing as professional detachment when it comes to your own child. In the investment realm however, market participants are consistently asked to defend their convictions, but also expected to be surgical about their losers. How can someone maintain enough attachment to weather rough times, but stay detached enough to surgically cut when necessary ?

“Cut your losers, run your winners” is the key to survival in the markets, but no-one tells You how to pick the lock. This is especially difficult if You are a fundamentalist (fundamental analyst/manager/investor/trader). First, there is no price mechanism like a stop loss to tell You it’s time to move on. Second, You don’t want to be perceived as lacking conviction. Third, investors want You to manage risk. No wonder 80% of managers find it difficult to outperform every year.

This is the second article in a series of four about exits and affective neurosciences. Our central premise is that the quality of exits will determine the quality of performance. The purpose of this exercise is to help fundamentalists cut their losers, run their winners, while keeping conviction. It is based on the assumption that they are refractory to the idea of a stop loss policy. It is a simple yet powerful method that is guaranteed to mechanically lift performance.

You do not need to be right 51% in order to make money

One of the classic myth is that “You will make money as long as You are right 51% of the time”. Wrong. You will make money only if You have a trading edge:

Trading edge = Average Win% * Win% – |Average Loss%| * Loss %

Let’s take an easy example: if average profit is twice as big as average loss, what would be the break-even hit ratio ?

0 = 2 * X – 1 *(1-X)

X = 1/3

with X = Win% and Loss% = 1- Win%

In a system with a 2/1 profit/loss ratio, you only need to be right 1/3 of the time. In other words, stock pickers who identify 3-5 baggers only need to keep losers small to make formidable gains

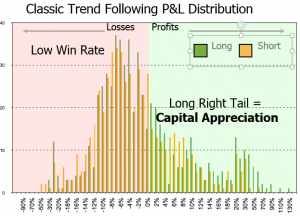

In reality, the visual representation of a stock picker’s P&L distribution looks very much like the chart below: a few princes make up for a lot of frogs. . Being right 51% of the time through the entire bull/bear cycle is the unicorn of stock picking. Every strategy experiences a drawdown at some point. Stock pickers make money as long as they stay disciplined and keep their losses small.

In order to move to the distribution shown below, one of two things need to happen:

- Either reduce the number of frogs: easier said than done, particularly when strategies stop working at some point through the cycle

- or, their impact is reduced: reducing drag will mechanically improve profitability

Predicting tomorrow’s winners is much harder than dealing with today’s losses. The game outlined below is an elegant way to deal with losers. Not only does it mechanically improve the trading edge, it also salvages ego and rewires neural pathways from outcome to process orientation.

The game of 2 halves

The objective is to halve the weight of losers once they detract more than half average contribution. Proceeds are then re-allocated to either fresh ideas or winners. This is a simple two-step process:

- Divide all positions between contributors and detractors, calculate average contribution: first half

- Reduce weight by half (1/2) for all detractors below -1/2*Average contribution: second half

Example:

Average contribution: +0.5% Babylon Ltd weight: 4% Unrealised P&L: -0.4% Realised P&L: 0%

After weight reduction Babylon Ltd weight: 2% Unrealised P&L: -0.2% Realised P&L: -0.2%

Now two things will happen: either Babylon Ltd will perish, or it will rise

- If Babylon meets a tragically eponymous fate : it would have to drop another -15%, just to reach minus average contribution, or -0.5%. At this point, it will be either it is a screaming Buy or a dog. Either way, it will be an easier decision to make

- If Babylon rises: then unrealised profits will compensate for realised losses. One rule of thumb in order to maintain a positive trading edge, do not add to the position until it crosses previous entry price

The additional 2% freed-up can be re-allocated either to winners or fresh ideas. Adding to winners cements conviction. Adding fresh ideas brings fresh blood to the portfolio. Either way, it is more of a good thing.

Special mention for managers who use an equal weight position sizing: Equal weight position has many drawbacks, but it has one benefit in this case. Instead of using contribution (weight * return), a simple distribution of return is sufficient.

The game of two halves has three deep benefits

- Trading edge mechanically improves: this is a simple elegant formulation of the first mantra: “cuts your losers and ride your winners”

- Good stewardship: managers are often torn between defending their convictions and dealing with problems. If they cut too frequently, they are perceived as lacking conviction, which negatively impacts investors confidence. By selling a portion of the position, they show peers and investors that they both maintain their conviction and deal with problems

- Process versus outcome neural pathways re-wiring: funds reach capacity not when they are too big in size, but when inertia sets in. Dealing with losers forces managers into action. This accomplishes three things:

- Managers become dispassionate with their problem children: since dealing with them improves stewardship, the stigma of taking a loss disappears. The game is simple enough to be executed even in the darkest

- Increased fluidity: since proceeds are re-invested, managers have a direct incentive to look for fresh ideas, or to their existing ones

- Process versus outcome mindset: believing that being right about a stock is a matter of profitability is an outcome process. When ideas are profitable, ego gets validation. When (not if) they are unprofitable, ego feels under attack. This invariably leads to defensive, unprofitable and often destructive behaviors. Dealing with losers in an orderly fashion changes focus from outcome to process. Being right is no longer about the outcome but about doing the right thing.

Conclusion

The game of two halves is a key to unlock the “Cut losers and ride winners” fortress. It is an elegant solution to the oldest problem in fundamental investment. It reconciles the demand for conviction with the need for action. The privilege of its (mathematical) simplicity is that it imposes itself even in the darkest times.

More importantly, it changes the definition of being right. It is not a binary outcome on the profitability of individual ideas., It is the observance of a process that will lead to higher aggregate profitability. In the Jungian archetypes, it no longer triggers the orphan (amygdala in the limbic brain, responsible for fight, fight or freeze), but activates the ruler (pre-frontal cortex or thinking brain). In short, the game of two halves reduces stress and improves profitability.

Thank you for your forum.Really thank you! Awesome. Studley

Stop loss is one of the primary element in day trading. Most people do not follow and in turn make huge losses

Thanks

Alliance Research

http://www.allianceresearch.in

researchalliancejbp@gmail.com