Finance is one industry where there is no shortage of creativity. There is always a new strategy, investment vehicle, or asset class. This alphabet soup is confusing, particularly when it comes to assessing risk and reward across asset classes. Yet, there is a simple universal way to classify strategies. They fall into two buckets: either mean reversion or trend following. Simply said, the exit policy determines the win rate, which then shapes the return distribution.

Over the years of patiently testing multiple algorithmic strategies, patterns in the return distribution repeated over and over. It eventually became apparent that strategies fall into two buckets: mean reversion or trend following. Attached are graphical representations of the gain expectancy of mean reversion and trend following strategies. The reason why the same patterns repeat themselves is simple: exit policy.

Market participants tend to treat exit as a single final event. Each trade is a binary event: either it is profitable or not. The accumulation shapes the return distribution. Hit ratio is then determined not by what we enter, but how we exit.

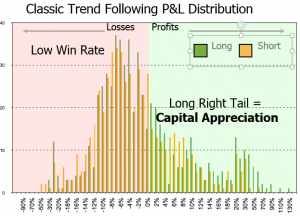

Charts below are return distributions for each strategy type. They are also visual representations of gain expectancy. One image speaks more than a thousand words. This representation changed my life. It permanently altered the way I perceive the markets. The game is about tilting gain expectancy: contain the left tail, moving the peak hit ratio to the right and elongating the right tail. This visual representation is a powerful tool. This is why we want to share it. We are committed to helping people build smarter trading habits. Sign-in to our newsletter (it’s free) and we will send you a portfolio diagnostic tool.

Examples of mean reversion strategies are

- Short Gamma: sell OTM options so as to collect pennies in front of a steam roller

- Pairs trading (non FX): bet on the convergence between two historically correlated securities

- Value investing: Buy low PBR stocks and “undervalued” assets

- Counter trend: sell short shooting stars and catch falling knives

Mean reversion strategies post modest but consistent profits. They cater to investors who would look for low volatility returns. Their challenge is the left tail, those infrequent big losses that will take a long time to recoup.

Trend following strategies have a few home-runs

Death by a thousand cuts: many frogs, a few princes

Trend following strategies rely on the capital appreciation of a few big winners. Whether they follow stories, fundamentals, earnings or price momentum, stock pickers are trend followers. They may fail to appreciate being called trend followers, but their P&L distribution tells a different story.

Trend followers kiss a lot of frogs: they have a low hit ratio, often between 30% and 45%. Performance is cyclical. Styles come in and fall out of favor. Volatility is elevated. Performance can be underwhelming for long periods of time. The key issue is to contain losses during drawdowns.

Trend following strategies share those common characteristics (see graphical representation):

- Relatively low turnover

- Low win rate: 30 to 40%: see chart

- Big wins and lots of small losses: right tail on chart

- Relatively higher volatility

- Pronounced cyclicality: style comes in and goes out of favor

Example of trend following strategies are

- CTA type systematic trend following,

- Momentum: earnings momentum, news-flow, price momentum

- GARP investing: growth at reasonable price

- Buy & hope

Trend following strategies post impressive but volatile performance. They can go through long periods of underwhelming performance, which take their toll on the emotional capital of managers. Their main challenge is to keep cumulative losses small. Profits only look big to the extent losses are kept small.

II. How to measure risk for each strategy type

Investors suffer from a “nice guy syndrome”: some young women genuinely say they want to marry a nice guy, but unconsciously react to so-called “bad boys”. Investors genuinely say they want returns, but in reality they do react to drawdowns. More specifically, they are susceptible to drawdowns in three ways:

- Magnitude: never lose more than what investors are willing to tolerate

- Frequency: lull investors to sleep. Clients will trade performance for low volatility: big money is fixed income, not stocks

- Period of recovery: never test the patience of investors.

There are two ways to lose a boxing match: either on points or by knock-out. Mean reversion strategies score until they get knocked out. Trend following strategies lose on points. Risk is not evenly distributed. Therefore, each strategy deserves its own set of risk metrics.

Risk metric for mean reversion strategies: knock-out

Knock-out

Mean reversion strategies have low volatility, consistent performance and high Sharpe ratio. On the surface, they are what investors look for. The problem is mean reverting strategies work well, until they don’t. Big losses are unpredictable. LTCM had a great Sharpe ratio, at least until October 15th, 1987… Risk is in the left tail. The best metric for mean reverting strategies is therefore: tail ratio. Tail ratio measures what happens at the ends of both tails:

Tail ratio = percentile(returns, 95%) / percentile(returns, 5%)

For example, a ratio of 0.25 means that losses are four times as bad as profits. Turnover then becomes an important variable: the higher the turnover the shorter the period of recovery. The two ways a mean reversion strategy can survive is either by 1) containing the left tail or 2) increasing turnover.

Mean reversion strategies will test investors’ nerves on two things: magnitude of loss and period of recovery. For example, some strategies such as fundamental pairs trading post constant, reassuring but modest profits like 0.5% a month. Then one day, they post losses of 3 to 5%. They lose in one month the gains of an entire year.

Investors often succumb to the sunk cost fallacy with mean reversion strategies. They believe that big losses are rare and that managers will eventually make them back. This bias ignores probabilities, particularly the theory of runs. It also ignores opportunity costs. The good news is that there is an optimal point below which it makes more sense to redeem than to stick with managers who experienced a severe loss. It is often referred to as

optimal stopping. Whilst the formula can be complicated, a simple rule of thumb is to redeem if losses are below 0.4 of turnover.

On the other, trend following strategies have tail ratios ranging from 3 to 10. Winners are much bigger than losers. So, tail ratio is meaningless for trend followers.

Risk metric for trend following strategies: erosion

Trend following strategies have typically low win rates. Risk is therefore not in the tails, but in the aggregates: are a few winners big enough to compensate for the multitude of losers ? Measuring risk then boils down a simple ratio of profits over losses. The risk metric for trend following strategies is therefore:

Gain to Pain Ratio = Sum(profits) / Sum(losses)

Trend following strategies will test investors nerves on frequency of losses and period of recovery. Frequency of losses is another word for volatility. Trend following strategies are volatile, but semi-volatility (downside volatility) is low. They can also post lackluster performance for long periods. For example, mutual funds have built-in cyclicality. Even if they claim to beat the index, mutual funds still lose money during bear markets.

GPR does not apply to mean reversion strategies because blow-ups are unpredictable. GPR can stay high until it is torpedoed by one or two bad losses.

Combined risk metric: Common Sense Ratio

“Common sense is not so common these days”, Voltaire, French freedom fighter

Managers rarely define themselves as adherents of either mean reversion or trend following. Even so, it still would not be easy to assess robustness. Besides, the more risk metrics we use, the more confusing it becomes. For example, some managers have great performance despite a bad Sharpe ratio, so the question is “which matters more in which context?”

Since both metrics outlined above can be expressed in a simple binary ratio, combining them makes sense. When this ratio was first to colleagues and friends in the HF world, comments sounded like “yep, common sense”, hence its imaginative name: Common Sense Ratio

Common Sense Ratio = Tail ratio * Gain to Pain Ratio

Common Sense Ratio = [percentile(returns, 95%) * Sum(profits) ] / [percentile(returns, 5%) * Sum(losses)]

Above 1: make money, below 1: lose moneyCSR is much more powerful than either metric taken individually.

Example 1: GPR = 1.12, TR = 0.25, turnover = 2, CSR = 0.275

Let’s take a classic mean reversion strategy that generates 10% p.a. (GPR = 1.1). It has a moderate turnover of 1.5. Within a 24 months period, it will post a monthly drop of -4%, with a 95% probability. This is 5 times as big as the average profit, and roughly 4 times as bad as right tail profits (TR = 0.25). Common Sense Ratio is CSR = 0.25 *1.1 = 0.275.

On the surface, it may look like a modestly attractive strategy. In reality, the period of recovery combined with magnitude of loss imply that investors will have to be patient. In very simple terms, the CSR shows that returns are not attractive enough to justify investing in such strategies. Try this with a few low volatility strategies. Risk is not where You think it is.

Example 2: GPR = 0.98, TR = 3, turnover = 0.5, CSR = 2.94

Now, let’s take a strategy that loses 2% over a complete cycle (GPR = 0.98). Best winners are 3 times as big as worst losers (TR = 3). Turnover is low 0.5. You may think, why invest in a vehicle that loses money ? It does not make sense. Yet, You are invested in such vehicles: welcome to the average mutual fund. 80% of mutual funds lose roughly 2% to the benchmark. Every now and then, they outperform with a vengeance. The rest of the time they suck air. Morality: over time, mutual funds are poor investment vehicles if You stay invested through the cycle.

III. How to tilt the win rate, gain expectancy and overall profitability depending on your win rate

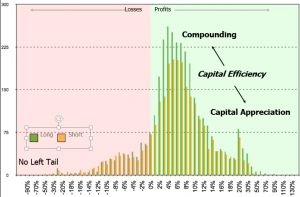

The question boils down to: is it possible to combine the benefits of both strategy types without having the drawbacks of either one ? How can we generate a return distribution that would look like the one on the chart ? (*)

The whole game of investing is about generating a return distribution that would have the following characteristics:

- No left tail: small losses like a trend following strategy

- Long right tail: big wins like a trend following strategy

- High win rate: above 50% win rate like a mean reversion strategy

This type of strategy combines both short term compounding with long-term capital appreciation.

Investors following a mean reversion typically come in early and leave too early. The key is therefore to elongate the right tail. This is done through allowing a remainder to extend beyond the mean with a trailing stop loss.

- Set a stop loss (more on this in an upcoming article)

- When the trade means reverts, close half the position

- Set a trailing stop loss (not based on valuation) and close the trade once the stop loss is penetrated

Bottom line, markets can stay irrational longer than You think. When it stops making sense for You, it may start making sense for someone else. Ride their tail, but protect your downside.

If You are a trend follower, here is a simple game (game of 2 halves) that will mechanically improve your return distribution. We all know that making money is about cutting the losers and riding the winners. Here is an objective way to do it:

- Calculate your average contribution, divide it by 2

- Reduce by half every losing position below – half average contribution

- re-allocate the proceeds to winners

Bottom line, you have reduced losers and increased winners in a simple way (more in an upcoming article)

Conclusion

The purpose of this article was to introduce a simple yet powerful way to reframe strategies independent of asset class. This enabled us to look at the merits and drawbacks of each type. We then looked at risk metrics that would best recapture their risk profile. We introduced a unified risk metric Common Sense Ratio that works across all asset classes. Finally, we looked at ways to tilt gain expectancy for each strategy type. Last but not least, if You want to know what your trading style, please subscribe and we will send You a diagnostic tool for free.

Preview of the next article:

The next article will deal with investor psychology. Short sellers have a unique perspective on investors psyche. We never sell short against buyers. We observe people who once held a position and are now processing grief. The next article will be about the psychology of grief adapted to the markets.

- Market regime: bear markets have several distinctive phases, with a measurable market signature

- You will never read an analyst report the same way again. You will learn to read emotions through language and back it up with numbers

- You will be better equipped to bottom fish for stocks

(*) : All above return distributions are derived from the same strategy. It has both mean reversion and trend following components. In order to draw a mean reversion strategy, the trend following component was switched off, and vice versa to build a TF distribution. Both components are normally switched on, third distribution

Answer by Laurent Bernut:

Answer by Laurent Bernut: