Our Research

The world does not need yet another market commentator. Our tools are designed to help investors along their investment journey

- Signals: trend reversal signals (Bull/Bear) on equity indices, Forex and government bonds

- Trading systems: simple steps from concept, back tests to auto-trade

- Money management: bet sizing algorithms, money/risk management tools

- Psychology: research and practical tools on habit formation

- Topics: discussions on the industry, trends

Trading Journal 2016/01/20

This is a test. If You find value in this trading journal, please let us know. If there are topics You would like to see covered, please comment and suggest. This journal exists only because You find it useful. So, help us create something You need.

1. No signals today

2. Trading activity Last night. Risk at this stage of a sell-off

3. General considerations:

- The vaporetto has left, there will be one coming soon: don’t short now, wait for the squeeze

- TIP of the day: counter-interintuitive truths about crowded shorts and performance during sell-offs (must read for novice short sellers)

- Position for the squeeze and beyond

Trading

Last night there was another Short EPOL, the ETF for Poland.

Here is how to read the chart:

Direction: Short. Comment: Trend is clearly fast bearish with low volatility. That trade has packed a lot of octane (reward to risk / holding period)

Stop Loss: 18.18

Target price: 15.97

Max Risk Per Trade suggested: -0.39% ( per convexity algo, not the standard -0.10% that will give readers a clean multiple). That is 95% of risk per trade

Trading Journal

RIsk: I elected to allocate -0.29% of risk. Risk is a number, not a dissertation. These are the reasons:

Pros:

- This is the third tranche. There is embedded risk free P&L of 0.53% that gives some cushion.

- More importantly, the lot size is such that only a small move is necessary to be able to cover a large portion and subsequently break even. It needs to generate 0.08% in order to reach break even level

- Current position before trade is getting small. It needs to be replenished

Cons:

- Trend is maturing. Borrow cost has increased accordingly. This is the third tranche in less than 4 months. Time for a break maybe ?

- Correlation increasing across asset classes, synchronous shorting is dangerous, so tone down the risk, take off -0.05%

- Rebound was small in duration and magnitude. It may be a false positive. In those fast trend it is either mid section, either before the rebound, take off -0.05%

Verdict: take the trade, but because of synchronous sell-off, reduce risk

3. General market considerations

If You haven’t shorted yet, it is too late. Vaporetto has left. Do not jump onboard now, You’ ll drown and feel stupid. Be patient, keep your powder dry.

Time is better spent observing the markets and observing your thoughts. Journal your thoughts. Observe the monkey on your shoulder.

Homework: this is a great time to get ready for the next campaign: (I have a system so I don’t need to do this anymore), but here is what I would look for: the weakest stocks that are not heavily shorted. Those are the stocks that Long holders sell.

Now is the time to think about the upcoming squeeze and beyond

The probability of a squeeze increases day by day. It is about time for a bit of mouth flapping. They call it reassuring the markets these days.

When they turned off free monetary booze, they expected a bit of weening turbulence, some whining, so no big deal so far.

Now that the vaporetto has left, let’s wait. When the squeeze comes, cover positions (half if You don’t have a system), or break even level if You use a similar equation as mine.

There is no need to cover it all. Markets have turned bearish, so the idea is to cover a portion, ride the squeeze and then slap another tranche.

Roadmap

When the squeeze is over, I will gross-up my leverage. At 127% Gross, -62% net, -22% net at risk today, I am under-participating. The idea was to start the year slow, build some performance cushion and gross up gradually. Bad idea to start sprinting at the beginning of a marathon.

So, when the squeeze comes, net at risk should drop to sub -10%. After the squeeze, gross up so that the net at risk be around -50/60%. This should be a gross of roughly 180-200% .

Now, life is usually what happens when You had other plans.

TIP of the Day: counterintuitive truth about short selling

You will usually find an inverse correlation with borrow utilisation level and performance in sell-offs. In other words, stuff that is heavily shorted all year round holds its ground during sell-off. Money is not made shorting the same stocks everyone shorts: Elvis has already left the building.

Money is made spotting the stocks that are not heavily shorted but underperform the markets. It makes counterintuitve sense: the market participants selling are Long holders selling their positions. Information has not traveled yet

These are the guys we will stalk, these are the guys whose coat we will tail. They are going through a process of grief: Denial, Anger, Bargaining, depression and acceptance. I quantified the process a few years ago. In fact, it was my first public speaking opportunity.

More about this and the Kubler Ross grief model applied to the markets on my website at www.alphasecurecapital.com . Please subscribe, It keeps me motivated. It is free and has resources for committed traders.

Conversely, make a note of the heavily shorted stuff that outperforms or holds its ground. This is squeeze box material where all the structural short sellers go impale themselves.

Short-selling: “Come with me if You want to live”

The 30s’ are usually remembered as the “Great Depression era”. Yet, from 1932 to 1937, despite abject poverty on main street, what was left of Wall Street enjoyed an exceptionally resilient bull market. The government had found a new tool called pump priming, inspired from an economist (only they can get away with such awful track records on the markets) named John Maynard Keynes. The government loved it and they feel asleep on the button. Sounds familiar ?

We have enjoyed a synchronous long smooth bull market. It has been good to all participants. Yet, no bull market has ever boosted anyone’s IQ. If anything, this Fed sponsored bull market has made participants fat and complacent: low interest rates pick up the tab anyway. Now, that the Fed has decided to tighten the purse, things may get a bit more turbulent out there.

Short-selling is the most underrated skill on the markets. It is neither a nefarious conspiracy nor an anti-patriotic gesture. It is a rare, versatile and immensely valuable craft that will ensure your survival in the most turbulent times. Markets have dropped by 50% twice in the last decade. If You would like to retire on returns rather than stories, then this is something worth learning.

Why You should listen to me ?

“Too many people look at “what is” from a position of “what should be”, Bruce Lee, Chinese philosopher

These days, everybody seems to have an opinion on short-selling. Short sellers seem to proliferate faster than syphilis on a ship. I cannot but feel humbled in such illustrious company. I have been in the alternative space for 15 years (hedge funds and large institutions). For the past 8 years, I was a dedicated short-seller with Fidelity Japan.

These days, everybody seems to have an opinion on short-selling. Short sellers seem to proliferate faster than syphilis on a ship. I cannot but feel humbled in such illustrious company. I have been in the alternative space for 15 years (hedge funds and large institutions). For the past 8 years, I was a dedicated short-seller with Fidelity Japan.

My mandate was to underperform the inverse of the longest bear market in modern history: Japan equities. Every day, I woke up -100% net short, having to do worse than the worst market on earth, good morning. These days, it feels somewhat refreshing to be around -50% net short.

While every other freshly minted guru has some elaborate speech about how short selling should be done, I have earned my short selling-skills the hard way and I have the scars to prove it. It is all lovely and cosy but the only tiny difference is that in the real world You can’t hit the reset button after Game Over. So, Come with me if You want to live

Why should You master the craft of short-selling ?

There are three obvious reasons:

- The secret to raising AUM is to perform when no-one else does. So, if You are a professional in the alternative space, just remember that when it is Babylon on the markets, investors will worship the Jamaican Prophet His Almighty Bob Marley

- Markets go up and markets go down: why not profit from both ? It takes a little more skill, that’s all

- A stronger version of yourself: In the world of short-selling, the market works against You. Either it will forge excellence out of You, either it will crush You. It is that simple. So, even if You decide to stay Long Only, learning to sell short will undoubtedly make You a formidable market participant.

Why do most people fail at short selling ?

“In theory, theory and practice are the same. In practice, they are not”, Yogi Berra, American Philosopher

Market participants approach short selling the same way they approach long buying. They do their analysis, watch some of it being validated and then happily conclude it is just the inverse of going long. That all works well until it is time to put theory into practice.

A couple of short-squeezes that would turn Barry White‘s rich baritone into Barry Gibb‘s high falsetto, a couple of quarters of humbling losses down the road, and they conclude that short-selling is dangerous. What they do not realise is that on the short-side, the market does not cooperate, stock picking is just not good enough. Market participants fail to understand the dynamics and the mechanics of short selling.

On the long side, picking stocks is sufficient. The market does all the heavy lifting thereafter. Stocks grow bigger, everything works in tandem: they contribute more both in terms of alpha and exposures. Losers shrink and hurt less.

On the short side, the market works against You. Winning big literally means watching your portfolio shrink like a magic skin: You have smaller victories when successful and bigger problems when unsuccessful.

Picking stocks is just the start. The real work of extracting alpha comes after that. This is hard, frustrating work, when it works at all. This is why people keep looking for structural shorts all the time, something they can sell short and throw away the key. Structural shorts are like market gurus, they are everywhere. Profitable structural shorts are more like market wizards, good luck finding one. They are so rare they make Big Foot look like a frequent guest on the Saturday Night Live show. Welcome to the mechanics of short selling: scarce poor quality borrow leading to short squeezes, prohibitive interest fees and dividends payable.

The MMA of short-selling

Martial arts are a good analogy for the markets. If Long only was a fighting sport, it would be English boxing, Queensburry rules. If Short selling was a sport, it would be MMA, Vale Tudo. Floyd Mayweather is the undefeated champion of the world. He is a solid contender for the title of the best boxer of all times. Yet, should he face Conor McGregor in the octagon, MMA style, he would be dismantled, dismembered and disfigured long before the first round bell has a chance to save him.

On the Long side, all You have to do is pick stocks and the market does the rest of the work for You.

On the short side, not only do You have to do that, but You will have to master those skills:

- position sizing: successful shorts shrink, unsuccessful ones hurt fast. Learn to size position so that they may contribute if successful, but not wound if not

- Milk your ideas: successful shorts shrink. So, it is not enough to find them, You must constantly work at them to extract alpha

- Consistent idea generation: a healthy short book shrinks, so You need to come up with at least twice as many ideas as the Long side just to keep up

- Market timing: two certainties in life: death and short squeezes a la Barry Gibbs. Use the latter for trading purposes before the former catches up

- Superior understanding of risk: risk is a number, not a pretty paragraph at the end of a dissertation. Short sellers naturally develop a keen understanding of hedges and probabilities.

- Process versus outcome thinking: if investment is a process then automation is a logical conclusion

- Mental fortitude: would You like to be the iceman on the trading floor when everyone else panics ? After a while, bull markets, bear markets, they all taste like chicken

The good news is that short-selling is a skill. It can be acquired, perfected and expanded. It is also a versatile and valuable one. Remember this: with this skill, You can go Long without breaking a sweat, but can Long-Only do your job with the same ease

How does it work in practice ?

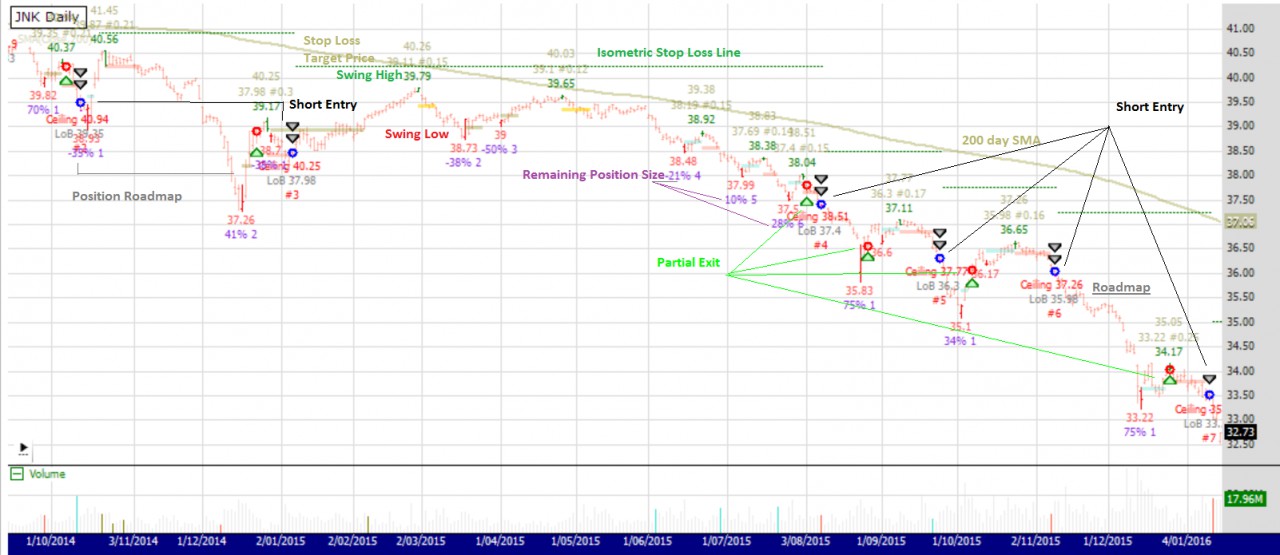

Short selling is a high pressure sport. Those who have only gone Long will suddenly be confronted with unfamiliar levels of stress. Volatility, uncertainty, fear, stress, pressure constrict the thinking brain (prefrontal cortex). Whatever mental bandwidth is left will be thankful for clear, unambiguous and simple instructions. So, do not be fooled by the apparent simplicity zen appearance of the charts. It took years to mature and thousands of lines of code to come to this level of clarity. In time, I hope You will learn to appreciate the gift of simplicity.

The above chart is designed to be intuitive.

- Price Bar colour: Down trends are coloured tomato. Uptrends are coloured olive. Back in 2012, the original name of the strategy was Olives & Tomatoes. (no wonder it initially failed to garner traction in my venerable institution…)

- Swings: swing high bars are coloured in green with a green annotation above the price bar. Swing low bars are coloured red annotation below the chart

- Annotations above/below swing bars:

- Olive (above) / Tomato (below):

- Stop Loss: Single number above/below all annotations

- Target price: target price is a risk management level. It is not an expression of fair value. Life is unfair, so are the markets, get over it

- #ATR: Average True Range [20 bars]

- Mauve (never trust a Frenchman with the colour code): Remaining balance. When engaged in a position, the algo calculates the quantity to exit so as to break even on the trade thereafter and prints remaining balance

- Olive (above) / Tomato (below):

- Dotted Green/Red Line: isometric staircase stop loss. Stop losses are reset for all positions. Those who fail to honour them will be unapologetically de-friended: may You be chained, eagles devour your liver and Justin Bieber fill your ears

- Black triangles: represent entries. Stacked triangles mean single entry, multiple exits. Above/Below is a precious roadmap that contain all the values for the journey ahead

- Ceiling/Floor: this is the equivalent of stop loss.

- LoB: is the equivalent of a Limit or Better price. Do not chase stocks past that point as probability recedes thereafter

- Red/Green inverted triangles: mean unprofitable/profitable exits. Stacked triangles mean final exits of multiple positions

- Moving Average: we all love our Christmas trees. This has no bearing on the strategy, but users have found it easier to anchor their beliefs around a long term moving average.

Charts have all the essential information You need to know to go on your journey: bullish/bearish underlying trend and exit roadmaps. It is kept simple by design. For example, position sizes have been removed in this version. They are calculated separately in the alert table. It all comes down to essentialist philosophy: focus on the essential few and let go of the trivial many. With this tool, You have a sustainable fighting chance against the markets.

Trading Journal

The above chart translates into real trading: multiple entries and exits. Green column is entry. Salmon is partial exit and grey is final exit. As soon as a position is entered, the first order of business is to take some money off the table so as to reduce risk.

Above is JNK, the ETF for high-yield bonds. When the first trade was taken, the chrematocoulrophony (chremato: money, phone: voice, coulro: clown) or consensus on The Street was talking about “Buy the dips”, “value hunting”. These days, everyone talks about the implosion of the high yield space. Bottom line, the hardest trades often offer the best rewards. Stick to your system.

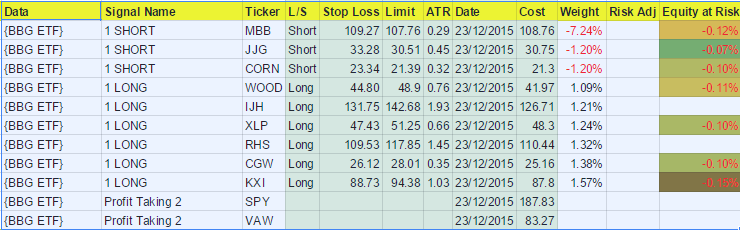

Alert table

The table contains the same information as charts, only in a more compact numerical form.

Types of Alert:

- Long Limit / Short Limit:

- Profit Taking: A swing has been recorded and the market is about to rebound/drop so time to take risk off the table. Exits are executed at market price: entry is a choice, exit is a necessity

- Trend reversal: Trend has changed from Bull to Bear and vice versa. Close open positions at market

- Stop Loss: remember the curse of Prometheus: liver may regrow, but Justin Bieber that is rough

- Weight: is derived from a fixed fractional position sizing method set at -0.10% (equity at risk method) for simplicity;s sake

That’s it, everyone is set. Happy trading. Two things, I trade the same signals that are shared on the website. Call it front-running or camaraderie. Rather than 5 pages of lawyerly bizantyne disclaimer, one sentence suffices: You are responsible for your own choices.

Conclusion

“The time to repair the roof is when the sun is shining”, JFK, modern mystery

Short-selling is a habit. It takes time, mistakes, patience to unlearn bad habits and form new beneficial neural pathways. The best time to do so is when urgency forces focus, but not critical enough to be a question of life and death.

The Fed has ended its life-support, which means more turbulence ahead. This is a good time to learn how to ride volatility with serene equanimity.

Why do 100% of economists say that it’s hard to predict stock prices?

Answer by Laurent Bernut:

Answer by Laurent Bernut:

“Forecasting is a difficult business, particularly when it is about the future”, Yogi Berra, modern American philosopherEconomists are extraordinarily helpful at predicting … the past. They will give today a savant explanation as to why their predictions for last week did not pan out. Economists gather some attention during bear markets when all predictions turned out be wrong anyways and investors want to gauge the “real economy”. Now, not only economists are wrong. Analysts are appalling and strategists are laughable. We, as a species, are biologically incapable of forecasting anything.Experts cannot predictIn early 2008, before the GFC, my friend Marco Dion, quants guru at JP Morgan, wrote a piece about analysts earnings forecast accuracy 1 year out.The probability of being spot on is a whooping 2%. The correct terminology for such low percentage is statistical error: “oops, I got it right”…The probability of being +/-10% was 25%. That is half a coin-toss.I used to compile strategists’ predictions published in Barrons and measure forecast accuracy twice a year. Fasten your seatbelt. If You thought analysts were bad, You haven’t seen anything yet. Forecast accuracy of Barrons roundtable was 17%. That is simply a few notches below useless, that is laughable.(The primary reason why strategists were so low is primarily the broad range of questions from interest rates to currency, S&P levels. Within their domain of competence (fixed income, equities or currencies), they were relatively OK but were tragic everywhere else)Why we can’t predictOur “ability to predict” is located in the prefrontal cortex. It is the siege of our thinking brain. Now, within that brain, there are several regions invoked every time we make a prediction.“High conviction” predictions trigger a zone called the ventro-median prefrontal cortex. The interesting part is the dorsolateral cortex, where our ego and identity gets activated. Hal Hershfield has observed through fMRI dual activation in those regions when subjects asked to make projections about their financial well being claimed to have good financial literacy. In other words, people who claimed they knew something about the subject were also more prone to overconfidence. Our forecasts are contextual.A third thing that makes it even more interesting is something called recency bias. We extrapolate tomorrow based on what we know today. Have You ever wondered why analysts earnings prediction go in straight line up through the next 20 years ? It does not even dawn upon them there could be a dip.Maybe we asked the wrong question in the first placeBack in the 60s, there were a series of studies conducted at Yale University where subjects were asked to send electric shocks to test subjects if they answered wrong (Milgram experiment ). Of course, test subjects were actors and no shocks were sent, but the interesting part was that few people rebelled. The objective was to measure compliance to authority, specifically how could people obey nazi orders and send victims to a certain death. We are conditioned to respect figures of authority and experts.

Yet, in finance, we still avidly seek the opinions of experts who continue to prove time and again that they are hopeless at it: they are still several standard deviations below a coin-toss. So, why do we still rely on them ?Rather than running an ugly contest on who’s worse at forecasting, maybe we should ask ourselves a better question: despite overwhelming evidence that we are hopeless at forecasting, why do we keep doing it ?Our fear receptor is a region in our brain called the amygdala. These are two glands in the center or our brain. They are our fear receptors. The amygdala has helped our ancestors survive saber tooth tigers. It has not evolved for thousands of years. In the Jungian and later Pearson Marr archetypes, amygdala could be compared to the orphan.Now, our primitive brain does not know the difference between a saber tooth in the bush and a news headline. Uncertainty triggers fear. This fear activates the amygdala.So, we rely on “experts” who know better and can reassure us and soothe our uncertainty. In other words, we delegate our fear management to experts.Is there a better way then ?Uncertainty is not going away anytime soon. Uncertainty and risk are part of life. Rather than delegating fear management, maybe we should learn to live with it, to make peace with it. Fear exists in the shadow and evaporates when brought to light.

- Mindful meditation: There are several techniques designed to reduce fear, one of the best being “mindfulness meditation”. I would also recommend the work of my trading coach Rande Howell (trader’s state of mind).

- Risk is a number: The second way is to quantify risk and stop loss. Risk is not a paragraph at the end of a dissertation called investment thesis. Risk is a number: know how much you are willing to risk and can afford to lose before entering any trade.

Conclusion“Forecasting is a difficult business, particularly when it is about the future”, Yogi Berra, modern American philosopherWe are hopeless at forecasting. Forecasts have been wrong and no matter how technology evolves, they are likely to be wrong in the future as well. (I had this conversation with Nate Silver in Hong Kong actually). Even if forecasts accuracy doubled, it would still be below a coin toss. So rather than trying to improve them, how about learning to live without them ? How about growing comfortable without discomfort ?If You are interested in how “Greed and Fear” tricks our brain: Amygdala and the neurophysiology of Greed and Fear. and, don’t forget to sign-up if You want to receive free bonus material

Why do 100% of economists say that it’s hard to predict stock prices?